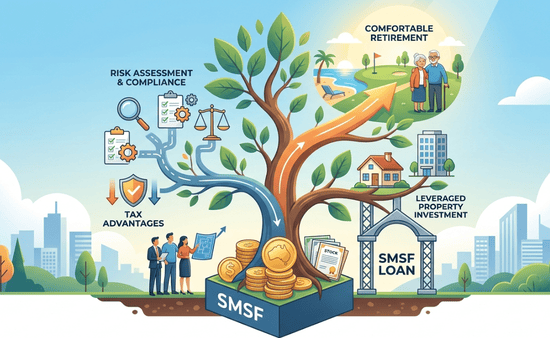

Preparing for retirement involves critical financial planning and strategic decision-making. Among the various options available for Australians to secure their financial future, self-managed super funds (SMSFs) have gained considerable attention. These funds not only offer greater control over retirement savings but also the opportunity to utilise smsf loans to maximise investment potential.

Understanding SMSF Loans

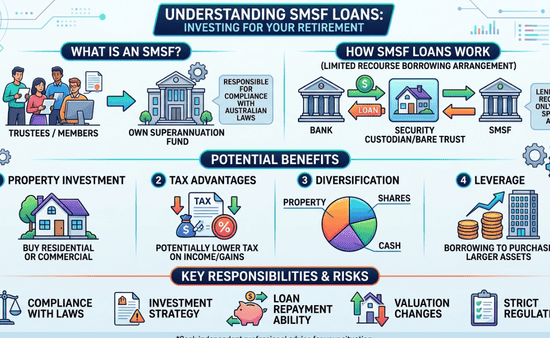

An SMSF allows members to be trustees of their own superannuation fund, giving them the responsibility to operate the fund according to Australian superannuation and taxation laws. Within the permissible framework, trustees can take out smsf loans to invest in authorised assets, which can include property and a range of other investment types.

SMSF loans can be a powerful financial tool for trustees seeking to invest in property as part of their diversified retirement strategy. The ability to leverage current superannuation funds to purchase a property that may appreciate over time can maximise the value of retirement savings. However, with great power comes great responsibility; hence, understanding the legal, regulatory, and financial implications of these loans is crucial.

Criteria and Limitations of SMSF Loans

There are specific criteria and limitations imposed on SMSF trustees looking to take advantage of smsf loans. The fundamental condition is that the loan must meet the ‘sole purpose test’, ensuring that the investment directly benefits fund members upon retirement or provides death benefits. Borrowing arrangements, often referred to as ‘limited recourse borrowing arrangements‘ (LRBAs), must adhere to stringent borrowing conditions laid out by the Australian Taxation Office (ATO) and other relevant legislation.

Additionally, the assets bought with loan funds must be held in a separate trust until the loan is paid off in full. This protects the rest of the SMSF’s assets in the event of a default. It is critical for trustees to stay informed about the potential risks and avoid over-leveraging their fund, which could jeopardise members’ retirement savings.

Benefits of Using SMSF Loans for Retirement

When utilised wisely, smsf loans can offer several benefits. The direct benefit is the capacity to make large-scale investments, like commercial or residential real estate, which may otherwise be unaffordable. The income generated from these assets, such as rental income, goes directly back into the SMSF, potentially increasing the fund’s size more rapidly than traditional saving routes.

Furthermore, there are tax advantages associated with SMSFs, including concessional tax rates on investment income and capital gains. In certain circumstances, this can result in a more tax-effective investment strategy compared to other borrowing methods.

Strategies for Optimising SMSF Loans for Retirement

To optimise SMSF loans for a comfortable retirement, careful planning and consideration of the following strategies are necessary:

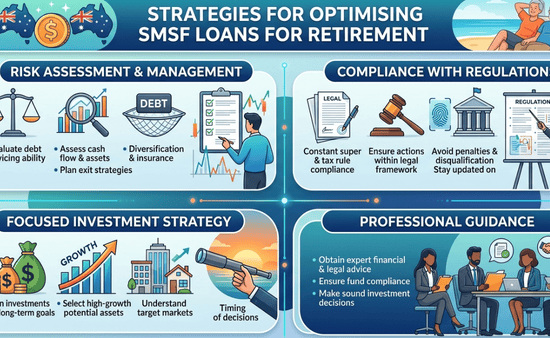

Risk Assessment and Management

Before taking out an SMSF loan, trustees must carefully evaluate their fund’s ability to service the debt. This includes assessing cash flow, existing fund assets, and an exit strategy should investments not perform as expected. It is also important to consider insurance and diversification to manage risks effectively.

Compliance with Regulations

Constant compliance with superannuation and taxation regulations is essential. Trustees should ensure that all their actions are within the legal framework to avoid penalties and possible disqualification of the SMSF. Staying up-to-date with the regulatory changes can be complex, so seeking professional financial advice might be beneficial.

Focused Investment Strategy

An effective investment strategy using smsf loans should consider the long-term goals of the fund. Investments should be selected based on their potential for growth and contribution to a comfortable retirement. Trustees must understand the market they are investing in and consider the timing of their investment decisions.

Professional Guidance

Given the intricacies involved in managing an SMSF and taking out loans, obtaining expert financial and legal advice is prudent. This helps ensure that the fund remains compliant and the investment decisions are sound.

The Role of Professional Advice in Managing SMSF Loans

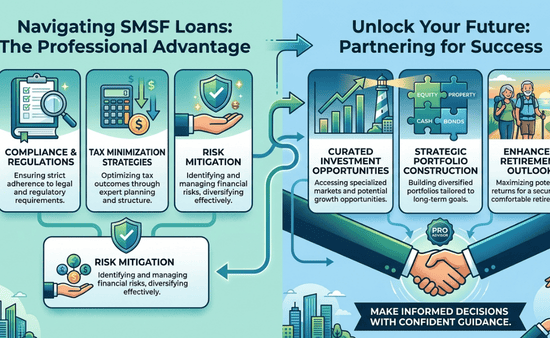

Professional advisers play a pivotal role in guiding trustees through the complexities of managing an SMSF and leveraging smsf loans effectively. Experts can offer insights into compliance, investment opportunities, tax implications, and risk management, which are invaluable to trustees.

Qualified advisers can also assist in constructing an investment portfolio that aligns with the fund’s goals and navigating the dynamic financial landscape. With their support, trustees can make informed decisions that could significantly enhance their retirement outlook.

Choosing the Right SMSF Loan Provider

Selecting the right loan provider is as important as any other decision regarding an SMSF. Trustees should look for reputable lenders with experience in SMSF loans who offer competitive rates and transparent terms. It’s recommended to evaluate multiple providers and understand the complete terms and conditions of the loan agreements.

Conclusion

SMSF loans represent a viable option for those looking to boost their retirement savings through strategic investment. While there are complexities and responsibilities associated with these loans, the potential benefits for a comfortable retirement can be significant when managed correctly. By staying informed, managing risks, complying with regulations, and seeking professional guidance, trustees can optimise their super funds and work towards ensuring a secure financial future.

For trustees considering this path, it’s essential to not only focus on the loan itself but also on the long-term retirement strategy it supports. With careful planning and the right professional advice, SMSF loans can be a valuable addition to your retirement financing toolkit.